Loan Origination System (LOS) in India

India’s digital lending industry is growing at an unprecedented pace. NBFCs, fintech companies, banks, MFIs, cooperative societies, and digital lenders are rapidly adopting automation to simplify and accelerate loan processing. Traditional manual loan processing methods are no longer capable of handling the growing demand for instant credit approvals, compliance management, fraud prevention, and customer experience.

This is where a modern Loan Origination System (LOS) becomes essential.

A Loan Origination System (LOS) is a technology platform that automates the complete loan journey — from borrower onboarding and document collection to underwriting, approval, disbursement, and compliance checks. Modern LOS platforms are designed to reduce manual work, improve operational efficiency, minimize fraud risks, and provide faster loan approvals.

Roopya offers an advanced AI-powered Loan Origination System in India specifically built for NBFCs, fintech lenders, banks, microfinance institutions, and digital lending startups. The platform enables lenders to automate the entire lending workflow while staying compliant with RBI digital lending regulations.

What is a Loan Origination System (LOS)?

A Loan Origination System (LOS) is software that manages and automates the end-to-end loan application lifecycle. It allows lenders to digitally process loan applications with minimal human intervention.

The LOS system handles:

- Digital borrower onboarding

- Online loan applications

- eKYC and document verification

- Credit bureau integration

- Automated underwriting

- Fraud detection

- Loan approval workflows

- Digital agreements and e-signatures

- Loan disbursement

- Compliance monitoring

The main purpose of an LOS is to reduce loan processing time, improve loan approval accuracy, and enhance customer experience.

Modern digital lending platforms in India now rely heavily on LOS technology to process personal loans, business loans, MSME loans, payday loans, gold loans, education loans, vehicle loans, and microfinance loans.

Why Loan Origination Systems Are Important in India

India’s lending ecosystem is rapidly digitizing due to:

- Rising fintech adoption

- Growth of online lending apps

- RBI digital lending guidelines

- Increased competition among NBFCs

- Growing customer demand for instant loans

- Expansion of UPI and digital banking

- Demand for paperless onboarding

Traditional loan processing methods involve manual paperwork, physical verification, lengthy approval timelines, and high operational costs. This creates delays and increases the risk of human error.

A digital LOS solves these challenges by automating every stage of the lending process.

Benefits include:

- Faster loan approvals

- Reduced operational costs

- Improved compliance

- Better fraud management

- Enhanced borrower experience

- Real-time analytics

- Scalable lending operations

According to industry discussions and fintech experts, lenders in India are increasingly prioritizing automation, API integrations, AI underwriting, and no-code workflow management when selecting LOS platforms.

Key Features of a Modern Loan Origination System in India

1. Digital Loan Application

A modern LOS enables borrowers to apply online through:

- Mobile apps

- Web portals

- APIs

- DSA portals

- Agent applications

Customers can upload documents digitally, complete applications remotely, and receive instant status updates.

This eliminates physical paperwork and branch dependency.

2. eKYC and Identity Verification

An advanced LOS integrates with:

- Aadhaar eKYC

- PAN verification

- DigiLocker

- CKYC

- Face verification

- OCR-based document scanning

This enables instant customer onboarding while complying with KYC and AML guidelines.

Roopya’s LOS supports automated KYC workflows and real-time verification APIs.

3. Automated Credit Underwriting

AI-powered underwriting is one of the most critical components of a modern LOS.

The system evaluates:

- Credit bureau scores

- Bank statements

- GST records

- Income patterns

- Alternative data

- Repayment history

- Risk behavior

Machine learning models help lenders make faster and smarter lending decisions.

Roopya integrates with all major Indian credit bureaus including CIBIL, Experian, Equifax, and CRIF.

4. Rule-Based Decision Engine

A rule engine automates loan approval logic using predefined conditions.

Example rules include:

- Minimum salary requirements

- Credit score thresholds

- Age eligibility

- FOIR calculations

- Employment checks

- Risk segmentation

This reduces manual underwriting dependency and increases approval consistency.

5. Fraud Detection System

Fraud prevention is extremely important in digital lending.

A robust LOS includes:

- Device fingerprinting

- Duplicate detection

- Geo-location checks

- Behavioral analytics

- Fake document detection

- Face matching

- Velocity checks

Modern fraud detection systems can significantly reduce loan default and fraud losses.

6. Workflow Automation

Workflow automation helps lenders create:

- Approval hierarchies

- Verification workflows

- Escalation rules

- Task management

- Automated notifications

This ensures faster processing and better operational control.

7. API Integrations

A scalable LOS must support API integrations with:

- Credit bureaus

- Payment gateways

- Banking systems

- Account aggregators

- eSign providers

- SMS gateways

- WhatsApp APIs

- Collection systems

- Accounting software

Roopya provides extensive API integrations for seamless lending operations.

8. Digital Agreement & eSign

Digital lending requires paperless agreements and electronic signatures.

LOS platforms integrate with:

- Aadhaar eSign

- Digital stamping

- eMandate systems

- eNACH providers

This accelerates loan disbursement and compliance management.

9. Real-Time Loan Tracking

Borrowers can track application status in real time, improving transparency and customer experience.

Lenders can monitor:

- Approval rates

- Conversion ratios

- Pending applications

- Disbursement timelines

- Operational productivity

10. Analytics & Reporting

Advanced LOS platforms provide:

- Portfolio analytics

- Risk analysis

- Branch performance reports

- Approval trends

- Collection forecasting

- Fraud reports

- Audit trails

Real-time analytics help lenders make data-driven decisions.

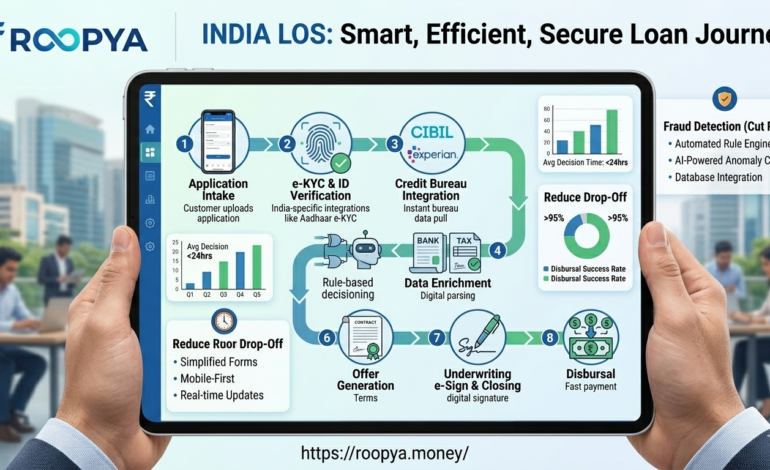

Loan Origination Process in India

Step 1: Loan Application

Borrowers submit applications online using mobile apps or websites.

Step 2: Document Upload

The system collects:

- Aadhaar

- PAN

- Salary slips

- Bank statements

- GST returns

- Business proof

Step 3: eKYC Verification

The LOS verifies customer identity using automated APIs.

Step 4: Credit Assessment

The system checks bureau scores, banking data, and risk parameters.

Step 5: Automated Underwriting

AI models and rules engines evaluate eligibility.

Step 6: Loan Approval

Approved applications move through workflow approvals.

Step 7: Digital Agreement

Borrowers complete eSign and digital documentation.

Step 8: Loan Disbursement

Funds are transferred directly to the borrower’s account.

Types of Lenders Using LOS in India

NBFCs

NBFCs use LOS systems to automate high-volume digital lending operations.

Fintech Companies

Fintech startups rely on LOS software for instant loan approvals and scalable growth.

Microfinance Institutions (MFIs)

MFIs use LOS systems to manage rural and micro-lending operations efficiently.

Cooperative Societies

Cooperative lenders use LOS platforms for member lending automation.

Banks

Banks implement LOS solutions to digitize retail and MSME lending.

Payday Loan Companies

Short-term digital lenders require ultra-fast loan processing systems.

Benefits of Loan Origination System for NBFCs

Faster Loan Processing

Modern LOS platforms reduce approval times from days to minutes.

Some advanced systems can process applications in under 30 seconds.

Lower Operational Costs

Automation reduces:

- Manual verification

- Branch dependency

- Documentation work

- Staffing requirements

This lowers per-loan processing costs significantly.

Improved Customer Experience

Borrowers prefer:

- Instant approvals

- Paperless onboarding

- Mobile applications

- Faster disbursements

Digital LOS systems improve customer satisfaction and retention.

Better Compliance Management

RBI regulations require lenders to maintain transparency and compliance.

An LOS helps lenders manage:

- Audit trails

- Consent management

- KYC compliance

- AML monitoring

- Data security

- Regulatory reporting

Reduced Fraud Risks

Advanced fraud analytics help lenders detect suspicious applications early.

Fraud management systems can reduce losses substantially.

Scalability

A cloud-based LOS allows lenders to scale operations without major infrastructure investment.

RBI Guidelines and Compliance for LOS in India

The Reserve Bank of India (RBI) has introduced strict digital lending guidelines to improve transparency and borrower protection.

LOS platforms in India must support:

- Consent-based data collection

- Secure customer data handling

- Transparent loan disclosures

- Audit logging

- Regulated digital onboarding

- Complaint management

- KYC and AML compliance

Compliance-ready LOS software is essential for licensed NBFCs and fintech lenders.

Reddit discussions and fintech communities increasingly highlight the importance of selecting RBI-compliant systems with strong governance and audit capabilities.

Cloud-Based LOS vs Traditional LOS

| Feature | Cloud-Based LOS | Traditional LOS |

|---|---|---|

| Deployment | Fast | Slow |

| Infrastructure Cost | Low | High |

| Scalability | High | Limited |

| Maintenance | Vendor-managed | Internal IT |

| Accessibility | Anywhere | Office dependent |

| Updates | Automatic | Manual |

| Security | Advanced cloud security | Depends on local infrastructure |

Cloud-based LOS platforms are becoming the preferred choice for Indian lenders.

AI in Loan Origination Systems

Artificial Intelligence is transforming digital lending in India.

AI-powered LOS platforms support:

- Predictive underwriting

- Fraud analytics

- Behavioral scoring

- Loan recommendation engines

- Automated verification

- Smart collections

AI models improve approval accuracy and reduce default risks.

Roopya’s AI-powered lending infrastructure helps lenders automate credit decisioning and risk assessment.

Challenges in Loan Origination

Fraudulent Applications

Digital lending fraud remains a major concern in India.

Regulatory Changes

RBI compliance requirements continue evolving.

Data Privacy

Lenders must ensure secure customer data management.

Integration Complexity

Multiple API integrations can create operational challenges.

Credit Risk Management

Thin-file borrowers require alternative underwriting approaches.

Why Choose Roopya Loan Origination System?

End-to-End Digital Lending Platform

Roopya provides a complete lending ecosystem for NBFCs and fintech companies.

AI-Powered Underwriting

Advanced machine learning improves loan decision accuracy.

RBI-Compliant Infrastructure

The platform supports regulatory compliance and audit management.

Fast Deployment

Lenders can launch quickly with cloud-based infrastructure.

API-First Architecture

Roopya integrates with major Indian fintech ecosystems.

Multi-Product Lending Support

Supports:

- Personal loans

- MSME loans

- Payday loans

- Gold loans

- Consumer finance

- Vehicle loans

- Microfinance loans

Real-Time Analytics

Comprehensive dashboards improve operational visibility.

Roopya Loan Origination System helps lenders automate and scale their lending business with secure, AI-powered, and compliance-ready infrastructure.

Future of Loan Origination Systems in India

The Indian lending ecosystem is expected to become increasingly digital and AI-driven.

Future LOS trends include:

- AI-based risk scoring

- Embedded finance

- Open banking integrations

- Hyper-personalized lending

- Real-time underwriting

- Blockchain-based verification

- Voice-enabled onboarding

- Predictive fraud analytics

Digital lending platforms will continue playing a critical role in financial inclusion and NBFC growth.

A modern Loan Origination System is no longer optional for lenders in India. It has become a critical technology requirement for NBFCs, fintech companies, banks, MFIs, and digital lenders looking to scale efficiently while maintaining compliance and operational control.

An advanced LOS automates the complete lending lifecycle — from onboarding and underwriting to approval and disbursement — while improving customer experience, reducing fraud risks, and accelerating loan approvals.

Roopya provides a next-generation AI-powered Loan Origination System built specifically for Indian lenders. With automation, API integrations, fraud prevention, analytics, and RBI-compliant infrastructure, Roopya helps financial institutions scale their digital lending operations faster and smarter.

==========================

FAQ

1. What is a Loan Origination System (LOS)?

A Loan Origination System (LOS) is software that automates the loan application, underwriting, approval, and disbursement process.

2. Who uses Loan Origination Systems in India?

NBFCs, fintech companies, banks, MFIs, cooperative societies, and digital lenders use LOS platforms.

3. What are the key features of a modern LOS?

Key features include:

- Digital onboarding

- eKYC verification

- Credit bureau integration

- AI underwriting

- Fraud detection

- Workflow automation

- Analytics dashboards

4. How does LOS improve loan processing?

LOS software reduces manual work, automates underwriting, accelerates approvals, and improves operational efficiency.

5. Is LOS software RBI compliant?

Modern LOS platforms are designed to support RBI digital lending guidelines, KYC compliance, and audit requirements.

6. Can LOS integrate with credit bureaus?

Yes, LOS systems integrate with CIBIL, Experian, Equifax, and CRIF.

7. What types of loans can be processed using LOS?

LOS platforms support:

- Personal loans

- MSME loans

- Payday loans

- Gold loans

- Vehicle loans

- Consumer finance

- Microfinance loans

8. Is cloud-based LOS better than traditional software?

Cloud-based LOS platforms offer better scalability, lower infrastructure costs, easier updates, and remote accessibility.