Why Your NBFC Needs Loan Origination Software in 2026

India’s lending ecosystem is changing at an unprecedented pace. The rapid growth of digital lending, AI-driven underwriting, instant approvals, and stricter compliance requirements has transformed how Non-Banking Financial Companies (NBFCs) operate. Customers no longer want to wait for days to receive loan approvals—they expect a seamless, digital-first experience with real-time updates and quick disbursements.

In 2026, relying on spreadsheets, paperwork, and disconnected systems is no longer enough. To stay competitive, NBFCs require an intelligent Loan Origination Software (LOS) that automates every stage of the lending lifecycle.

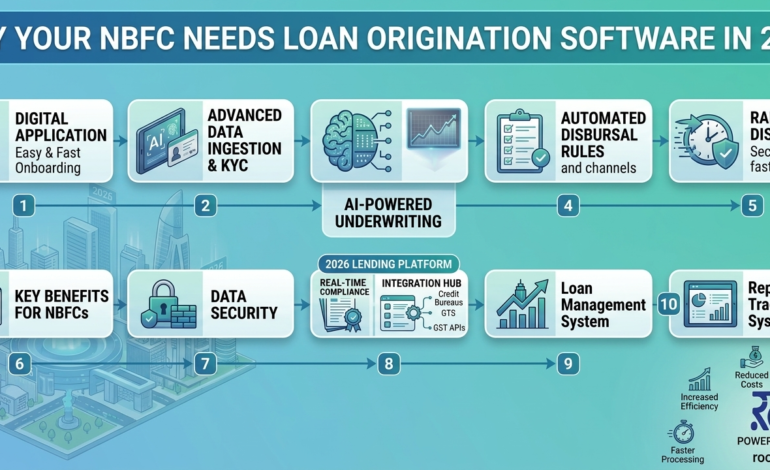

Modern platforms like Roopya’s Loan Origination Software provide end-to-end automation, from borrower onboarding and KYC verification to credit assessment, underwriting, approvals, documentation, and loan disbursement. According to Roopya’s platform information, it is designed as a cloud-based, AI-enabled lending infrastructure with workflow automation, business rule engines, digital onboarding, and analytics capabilities.

This article explains why every forward-looking NBFC should invest in Loan Origination Software in 2026.

What is Loan Origination Software?

Loan Origination Software (LOS) is a technology platform that automates the complete loan application and approval process.

It manages:

- Customer onboarding

- Digital KYC

- Document collection

- Credit bureau verification

- Underwriting

- Risk assessment

- Approval workflows

- Sanction generation

- E-signatures

- Loan disbursement

Instead of handling multiple systems manually, lenders can manage the entire origination journey from a centralized dashboard.

Why 2026 is a Turning Point for NBFCs

The lending industry is becoming increasingly technology-driven.

Several trends are reshaping the market:

- AI-powered credit decisioning

- Paperless onboarding

- Mobile-first customer experiences

- API-based integrations

- Automated compliance

- Real-time analytics

- Faster loan approvals

- Cloud-native infrastructure

Customers compare lenders based on speed and convenience. If your NBFC still depends on manual processes, it risks losing customers to digital competitors.

Challenges Faced by Traditional NBFC Operations

Many NBFCs continue to experience problems such as:

Manual Documentation

Physical paperwork increases processing time and introduces errors.

Delayed Loan Approvals

Manual verification often extends turnaround times from hours to days.

High Operational Costs

Staff spend significant time on repetitive tasks like document validation and data entry.

Compliance Risks

Regulatory requirements demand consistent KYC, audit trails, and secure data management.

Poor Customer Experience

Borrowers expect digital applications, instant status updates, and minimal paperwork.

Benefits of Loan Origination Software for NBFCs

1. Faster Loan Processing

Automation significantly reduces processing time.

Instead of manually reviewing every application, predefined workflows route files automatically.

This enables:

- Same-day approvals

- Faster underwriting

- Quick disbursement

- Reduced customer drop-offs

2. Automated Digital Onboarding

Borrowers can complete the entire process online.

Features include:

- Online application forms

- Aadhaar verification

- PAN validation

- OCR document capture

- Digital signatures

- Video KYC

This eliminates branch visits and accelerates onboarding.

3. AI-Based Credit Assessment

Artificial Intelligence improves lending decisions by analyzing:

- Credit history

- Income patterns

- Banking transactions

- Employment information

- Alternative data sources

AI helps lenders reduce defaults while approving deserving applicants faster.

4. Built-In Business Rule Engine

Every NBFC follows unique credit policies.

Loan Origination Software allows lenders to configure:

- Eligibility criteria

- Loan limits

- Approval matrices

- Product-specific rules

- Risk thresholds

Automation ensures consistency across every application.

5. Reduced Operational Costs

Automation minimizes manual work across departments.

Employees can focus on:

- Customer acquisition

- Portfolio growth

- Credit strategy

- Collections optimization

Lower operational costs improve profitability.

6. Improved Compliance

Regulatory compliance is becoming increasingly important.

Modern LOS platforms maintain:

- Audit logs

- Role-based access

- Digital records

- Secure document storage

- Automated KYC workflows

This reduces compliance risks and improves transparency.

7. Better Customer Experience

Today’s borrowers expect instant digital services.

Loan Origination Software offers:

- Mobile applications

- Online status tracking

- Automated notifications

- Paperless documentation

- Faster approvals

A better customer journey improves conversion rates.

Why Cloud-Based Loan Origination Software Matters

Cloud infrastructure provides:

- Remote accessibility

- Automatic updates

- Enterprise security

- Easy scalability

- Lower IT costs

- Business continuity

Growing NBFCs can expand without investing heavily in infrastructure.

AI is Transforming Loan Origination

Artificial Intelligence is redefining lending.

Key AI capabilities include:

Automated Underwriting

Applications are evaluated within minutes using predefined risk models.

Fraud Detection

AI identifies suspicious patterns before loan approval.

Predictive Risk Analysis

Machine learning estimates repayment probability based on multiple data points.

OCR-Based Document Processing

Identity documents are extracted and validated automatically.

Digital Lending Requires End-to-End Integration

Modern Loan Origination Software integrates with:

- Credit bureaus

- Payment gateways

- Banking APIs

- e-KYC providers

- Account aggregators

- GST verification

- PAN verification

- Aadhaar authentication

Connected ecosystems eliminate manual intervention.

Loan Origination Software Improves Scalability

As loan volumes increase, manual teams struggle.

LOS enables NBFCs to process thousands of applications with standardized workflows.

Benefits include:

- Consistent approvals

- Faster expansion

- Lower hiring costs

- Better monitoring

- Centralized operations

Data Analytics Drives Better Lending Decisions

Built-in dashboards provide insights into:

- Approval ratios

- Rejection reasons

- Processing timelines

- Portfolio performance

- Branch productivity

- Customer acquisition

Data-driven decisions improve long-term growth.

Why Roopya is an Ideal Choice for NBFCs

Roopya provides a comprehensive digital lending platform built specifically for Indian lenders.

According to its platform information, Roopya offers:

- Cloud-native Loan Origination Software

- AI-powered underwriting

- Digital borrower onboarding

- No-code business rule engine

- Multi-bureau integrations

- OCR-based document verification

- Workflow automation

- Lending analytics

- Loan Management System integration

- API-driven architecture

Its platform is designed to help NBFCs automate origination while supporting scalability and regulatory readiness.

Key Features Every NBFC Should Look For

When choosing Loan Origination Software, ensure it includes:

- AI underwriting

- Business Rule Engine

- Digital KYC

- OCR document processing

- Workflow automation

- Mobile onboarding

- API integrations

- Cloud deployment

- Compliance management

- Analytics dashboards

- Multi-product support

- Loan Management System integration

Future Trends for Loan Origination in 2026

The lending industry will continue evolving through:

- Hyper-automation

- AI-driven decision engines

- Embedded finance

- Open banking integrations

- Real-time credit scoring

- Digital identity verification

- Predictive analytics

- API-first ecosystems

NBFCs adopting these technologies early will gain a competitive advantage.

The future of lending belongs to organizations that can combine speed, compliance, automation, and superior customer experiences.

For NBFCs, Loan Origination Software is no longer an optional technology investment—it is a strategic necessity. By replacing manual workflows with intelligent automation, lenders can reduce turnaround times, improve operational efficiency, strengthen risk management, and deliver a seamless borrower journey.

As digital lending accelerates in 2026, adopting a modern platform such as Roopya can help NBFCs scale confidently while remaining agile in a competitive market.

Frequently Asked Questions (FAQs)

1. What is Loan Origination Software?

Loan Origination Software is a digital platform that automates the complete loan application, verification, underwriting, approval, and disbursement process.

2. Why do NBFCs need Loan Origination Software in 2026?

NBFCs need LOS to automate lending operations, improve customer experience, reduce costs, strengthen compliance, and accelerate loan approvals.

3. What is the difference between Loan Origination Software and Loan Management Software?

Loan Origination Software manages the pre-disbursement process, while Loan Management Software handles repayments, servicing, collections, and post-disbursement activities.

4. How does AI improve loan origination?

AI automates underwriting, detects fraud, analyzes borrower risk, processes documents using OCR, and helps lenders make faster and more accurate decisions.

5. Can Loan Origination Software integrate with credit bureaus?

Yes. Modern LOS platforms integrate with multiple credit bureaus, KYC providers, payment systems, and banking APIs.

6. Is cloud-based Loan Origination Software secure?

Yes. Reputable cloud-based solutions provide encryption, role-based access, audit logs, backups, and enterprise-grade security.

7. Does Loan Origination Software support multiple loan products?

Yes. Most enterprise LOS platforms support personal loans, business loans, MSME loans, gold loans, vehicle loans, and other customized lending products.

8. How does Roopyya help NBFCs?

Roopya provides AI-powered loan origination, digital onboarding, workflow automation, analytics, and integrated lending infrastructure tailored for Indian financial institutions.