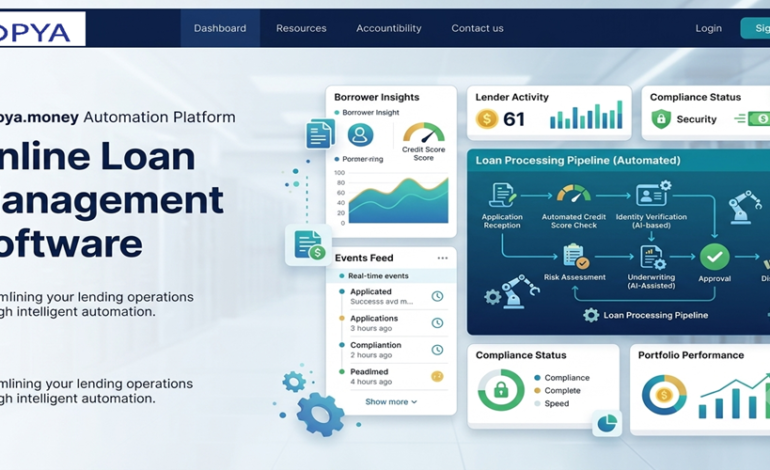

Online Loan Management Software: The Complete Guide for Modern Lenders

Managing loans after disbursement is where many lending businesses quietly bleed efficiency. Applications get lost in spreadsheets, repayment schedules are manually tracked, collections teams operate without data, and regulatory reports are assembled from a patchwork of disconnected systems. This is exactly the problem online loan management software exists to solve — and it is exactly what Roopya was built to do.

Whether you are a growing NBFC in India, a microfinance institution, a cooperative bank, or a fintech lender scaling your portfolio, having the right loan management system (LMS) is not a luxury — it is infrastructure. This guide covers everything you need to know about online loan management software: what it is, what it does, how to evaluate it, and why Roopya’s platform is the benchmark that modern lenders are choosing.

What Is Online Loan Management Software?

Online loan management software is a digital platform that enables financial institutions to manage the entire post-disbursement lifecycle of a loan. Once a loan is approved and funds are released, the loan management system takes over — handling everything from generating repayment schedules to tracking EMIs, managing prepayments, monitoring delinquencies, executing collections, and producing compliance-ready reports.

Unlike traditional loan management that relied on physical ledgers, Excel sheets, or legacy desktop applications, online loan management software operates in the cloud. This means lenders access it through a browser or API, data is updated in real time, teams across locations can collaborate on a single source of truth, and the system scales without infrastructure investment.

In India’s rapidly growing lending market — where NBFCs, MFIs, and fintechs are disbursing lakhs of loans every month — a robust online loan management system is the backbone of a sustainable, compliant, and profitable lending operation.

Why Loan Management Is More Complex Than Loan Origination

Most fintech conversations focus heavily on customer acquisition and loan origination — the front end of lending. But seasoned lenders know that the post-disbursement phase is where operational complexity truly lives.

Consider what happens after a loan is disbursed. The system must calculate and communicate repayment schedules to borrowers.

Do this for hundreds of borrowers and it is manageable with manual processes. Do it for thousands — which is the reality for any lending business with ambitions — and manual processes collapse under their own weight. Errors multiply, regulatory exposure grows, collections suffer, and the borrower experience deteriorates.

Online loan management software is built specifically to handle this operational complexity at scale, with accuracy, speed, and compliance built in.

Core Features of Online Loan Management Software

1. Automated Repayment Schedule Generation

The moment a loan is disbursed, the system should automatically generate a complete amortization schedule — principal, interest, processing fees, applicable taxes, and due dates — based on the loan product’s configured parameters. Roopya’s LMS does this instantly for all standard loan types: flat rate, reducing balance, step-up EMI, bullet repayment, and custom structures.

Lenders configure their loan products once in the system; every new disbursement under that product inherits the correct calculation logic automatically, eliminating manual errors in schedule generation.

2. Multi-Channel Payment Processing

Borrowers today expect to pay via NEFT, RTGS, UPI, NACH mandate, payment gateways, and even cash at branches. Online loan management software must support all these channels, automatically reconcile payments received, and update the borrower’s ledger in real time.

Roopya integrates with 300+ pre-built APIs including leading payment gateways and NACH platforms, so incoming payments are matched to the correct loan account and EMI allocation is calculated automatically — principal first or interest first, per your product policy.

3. Loan Account Ledger Management

Every loan in your portfolio is a live financial instrument. The system must maintain a precise, audit-ready ledger for each account: opening balance, disbursements, accrued interest, payments received, overdue charges, waivers, prepayments, adjustments, and closing balance — updated in real time.

A well-designed LMS presents this ledger transparently to both the lender’s back office and the borrower through a self-service portal, reducing inbound customer queries significantly.

4. Delinquency Tracking and Aging Reports

One of the most critical functions of any loan management system is monitoring the health of the portfolio in real time. The system must track Days Past Due (DPD) for every account, automatically age accounts into DPD buckets (0, 30, 60, 90, 90+), and surface these to operations teams in real time.

Roopya’s LMS provides live delinquency dashboards, configurable DPD bucket views, and aging reports that can be exported for board reviews, regulatory submissions, or internal risk meetings.

5. Collections Management

Delinquency tracking is only useful if it triggers action. Roopya’s online loan management software integrates a built-in collections engine that automatically initiates workflows when an account goes overdue. Automated SMS and email reminders go out on configurable days before and after the due date. Overdue accounts are assigned to collections agents based on configurable rules — by geography, bucket, amount, or relationship. Agents see their assigned queue through a dedicated collections interface, can log call outcomes, and can initiate payment plans or settlement offers within policy boundaries.

6. Prepayment and Foreclosure Management

Borrowers often want to pay more than their EMI or close their loan early. The system must handle these scenarios accurately: recalculating the outstanding principal, applying prepayment charges (if any) per product policy, regenerating the amortization schedule for partial prepayments, and processing full foreclosure with the appropriate charges and a final settlement letter.

Doing this manually is error-prone and time-consuming. Roopya’s LMS processes prepayments and foreclosures automatically, with the option for back-office approval workflows for amounts above defined thresholds.

7. NPA Classification and Provisioning Support

For regulated lending institutions, NPA (Non-Performing Asset) classification is a mandatory and auditable process. The system must automatically classify accounts as Standard, Sub-Standard, Doubtful, or Loss based on DPD rules mandated by the RBI or applicable regulator, and calculate required provisioning amounts.

Roopya’s LMS automates NPA classification and generates provisioning reports that support your accounting and compliance teams with accurate, real-time data.

8. Restructuring and Rescheduling

Loan restructuring — extending tenure, reducing interest rate, offering moratorium periods — is sometimes necessary for portfolio health. Online loan management software must support these operations without data loss, maintaining a complete audit trail of the original terms, the restructuring event, and the revised schedule.

Roopya supports configurable restructuring workflows with checker/maker controls, ensuring restructuring decisions are documented, authorized, and auditable.

9. Customer Self-Service Portal

Borrowers today expect digital access to their loan information. A built-in customer portal — accessible via web or mobile — allows borrowers to view their outstanding balance, download their repayment schedule, see their payment history, download NOCs or statements, and make payments directly. This reduces operational load on your customer service team and improves borrower satisfaction.

10. Regulatory Reporting and Compliance

For NBFCs and banks, regulatory reporting is non-negotiable. The LMS must produce RBI-mandated reports, GST reports, and data formats required for credit bureau reporting to CIBIL, Experian, CRIF, and Equifax. Roopya’s compliance engine is continuously updated to reflect changes in regulatory requirements, ensuring your submissions are always accurate and on time.

The Business Case for Investing in Online Loan Management Software

Lenders who deploy a modern online loan management system — as opposed to managing loan servicing manually or with legacy tools — consistently report measurable improvements across key operational metrics.

Reduced cost per loan serviced. Automation of repayment processing, EMI allocation, and account updates eliminates the need for large back-office teams performing manual data entry. Lenders typically see 40–60% reduction in operational costs per loan after deploying a modern LMS.

Improved collection efficiency. Automated reminders and structured collection workflows mean more payments are received on time without agent intervention, reducing delinquency rates. When human intervention is needed, agents have complete, real-time information rather than guessing from stale reports.

Better portfolio visibility. Leadership teams need real-time visibility into portfolio health. Online loan management software provides dashboards and reports that surface concentration risks, early warning signals, and performance metrics — enabling proactive decisions rather than reactive firefighting.

Regulatory confidence. Manual compliance processes create audit risk. An automated LMS generates accurate, consistent, and audit-ready regulatory reports, reducing the risk of regulatory penalties.

Faster borrower resolution. When a borrower calls with a query about their account, your team needs instant access to accurate data. A modern LMS surfaces complete account history in seconds, reducing average handle time and improving borrower experience.

Scalability. Manual loan management does not scale. With online software, adding 10,000 new loans to your portfolio does not require adding 10,000 units of manual effort — the system handles the growth automatically.

Who Needs Online Loan Management Software?

NBFCs (Non-Banking Financial Companies)

NBFCs are among the most active users of online loan management software in India. Whether you offer personal loans, business loans, two-wheeler loans, gold loans, or microfinance products, an LMS is essential for managing your portfolio efficiently while staying compliant with RBI’s Master Directions.

Microfinance Institutions (MFIs)

MFIs typically manage very high volumes of small-ticket loans — often to group borrowers in rural or semi-urban areas. The collection frequencies are often weekly or fortnightly rather than monthly. Online loan management software built for MFIs must handle these nuances: group loan structures, field collection workflows, and rural network conditions.

Banks and Cooperative Banks

Banks have strict regulatory oversight and complex product structures. Their LMS needs to handle multiple loan types simultaneously, integrate with core banking systems, support NPA provisioning, and produce reports in exact RBI formats.

Fintech Lenders

Fintech lenders typically process high volumes at speed, with strong API-first requirements. They need an LMS that integrates cleanly with their tech stack, supports automated decisions, and scales without friction.

Loan Service Providers (LSPs)

LSPs who originate loans on behalf of regulated lenders need transparent, real-time access to portfolio data — including disbursements, repayment status, and collections — to service their lending partners effectively.

What Makes Roopya’s Online Loan Management Software Different

Roopya is not just another loan management system. It is a unified, no-code lending infrastructure platform purpose-built for the Indian market, designed to get lenders operational faster, at lower cost, and with more flexibility than any competing solution.

No-Code Configuration

Every loan product parameter — interest calculation method, repayment frequency, charge structures, prepayment rules, NPA classification criteria — is configurable through Roopya’s intuitive no-code interface. There is no need to raise IT tickets or wait for developers when you want to launch a new product or modify an existing one.

Go Live in 1 Day

Roopya’s streamlined onboarding means lenders can get their LMS fully configured and operational within a single business day. For a growing NBFC or a new fintech lender, this speed to market is a decisive competitive advantage.

Pay As You Use

Traditional LMS vendors charge large upfront licensing fees, implementation costs, and annual maintenance charges that burden early-stage lenders with fixed costs before they have achieved scale. Roopya’s pricing model eliminates upfront costs — you pay based on actual usage, making it equally accessible for a lender disbursing 100 loans per month and one disbursing 100,000.

300+ Pre-Integrated APIs

Roopya comes pre-integrated with over 300 APIs covering payment gateways, NACH providers, credit bureaus, KYC and verification services, eSign platforms, and communication tools. This means your LMS connects to your payment collection infrastructure out of the box, without custom integration projects.

AI-Powered Intelligence

Roopya’s LMS is enhanced with AI capabilities that go beyond basic automation. Machine learning models analyze repayment behaviour to generate early warning signals before accounts become delinquent. AI-driven collection scoring helps prioritize collection effort for maximum recovery. Automated insights surface portfolio trends and risk concentrations that manual analysis would miss.

Integrated Collections Engine

Unlike many LMS platforms that require a separate collections system, Roopya’s LMS includes a fully integrated collections engine with automated reminders, configurable collection workflows, agent assignment rules, call outcome tracking, and payment plan management — all within a single platform.

Regulatory Compliance Built In

Roopya’s compliance engine is continuously updated. Credit bureau reporting formats, RBI regulatory reports, GST calculations — all are maintained by Roopya’s team and updated as regulations change, so your lender is always compliant without manual effort.

Complete Audit Trail

Every action in Roopya’s LMS — every payment processed, every account modification, every waiver granted, every restructuring decision — is logged with timestamp, user identity, and before/after values. This audit trail satisfies the most rigorous regulatory or internal audit requirements.

Roopya LMS: Key Modules at a Glance

| Module | Key Capabilities |

|---|---|

| Loan Account Management | Ledger maintenance, interest accrual, payment allocation |

| Repayment Scheduling | Amortization for all loan types, configurable frequencies |

| Payment Processing | Multi-channel integration, auto-reconciliation, real-time updates |

| Collections Engine | Automated reminders, agent workflows, payment plans |

| Delinquency & NPA | DPD tracking, bucket aging, NPA classification, provisioning |

| Prepayment & Foreclosure | Automated calculation, approval workflows, settlement letters |

| Customer Portal | Self-service access, payment, statements, NOC download |

| Regulatory Reporting | RBI reports, credit bureau uploads, GST compliance |

| Analytics & Dashboards | Portfolio health, performance metrics, trend analysis |

| Early Warning System | Predictive default signals, behavioral analytics |

Implementation: How Roopya Gets You Live Faster

A common fear among lenders evaluating new software is implementation complexity. How long will it take? How much will it disrupt existing operations?

Roopya’s implementation philosophy is designed to minimize all of these concerns.

For new lenders, Roopya provides pre-configured loan products and customer journeys that can be adapted to your specific product specifications through the no-code interface — no development required, go-live in a day.

Integration Ecosystem

Roopya’s online loan management software integrates with the entire ecosystem of tools that modern Indian lenders depend on:

Payment & Collections: Razorpay, PayU, Cashfree, EnachNACH, Digio eNACH, Yes Bank NACH, and more.

Credit Bureaus: CIBIL, Experian, CRIF Highmark, Equifax — for both pre-disbursement bureau pulls and post-disbursement credit reporting.

Communication: SMS, WhatsApp, email via leading providers for automated borrower communication and collection reminders.

eSign & Digital Documentation: Aadhaar eSign, DSC-based signing, digital agreements.

KYC & Verification: Aadhaar verification, PAN verification, GST verification, bank account verification, video KYC.

Accounting: Export integrations with leading accounting platforms for seamless reconciliation.

Security and Data Privacy

Loan management data is among the most sensitive financial data that exists. Roopya’s platform is built with security as a foundational requirement, not an afterthought.

Data is encrypted at rest and in transit using industry-standard encryption. Access controls are role-based, ensuring each user sees only the data relevant to their function. Multi-factor authentication protects system access. All processing happens on secure, compliant cloud infrastructure. Roopya maintains data residency within India, ensuring compliance with India’s data localisation requirements.

Customer Success: Why Lenders Trust Roopya

Roopya is trusted by a growing community of modern lenders across India — from early-stage NBFCs deploying their first digital loan product to established institutions scaling their portfolio with more intelligent operations. Customers like IndiaKaLoan, QuickFinShop, EazyCredit, and Findoc have chosen Roopya as their lending infrastructure partner, citing the speed of deployment, the depth of functionality, and the responsiveness of the Roopya team as key differentiators.

Getting Started with Roopya’s Online Loan Management Software

The best way to evaluate Roopya’s LMS is to see it in action. Roopya offers a personalized demo where the team walks you through the platform configured for your specific loan products, portfolio size, and operational requirements.

There is no lengthy RFP process, no months-long implementation, and no large upfront commitment required. You can go live in a day and pay based on what you use.

To schedule your demo, visit roopya.money/contact-us or reach out directly to the Roopya team.