How to Choose Loan Origination Software: A Complete Guide for Modern Lender

The lending industry has undergone a massive digital transformation over the last decade. Traditional paper-based loan processing methods are rapidly being replaced by intelligent digital lending platforms that automate borrower onboarding, credit assessment, underwriting, approval workflows, compliance checks, and loan disbursement.

For NBFCs, banks, microfinance institutions, cooperative lenders, and fintech companies, choosing the right Loan Origination Software (LOS) is one of the most important technology decisions they will make.

A Loan Origination System serves as the backbone of lending operations. It directly impacts operational efficiency, customer experience, approval turnaround time, risk management, regulatory compliance, and business scalability.

However, with dozens of LOS vendors in the market, selecting the right solution can be overwhelming.

This guide explains everything lenders need to know about choosing Loan Origination Software and the key factors that should influence their decision-making process.

What is Loan Origination Software?

Loan Origination Software is a digital platform that automates and manages the complete loan lifecycle from application submission to loan disbursement.

A modern LOS helps lenders streamline:

- Lead management

- Borrower onboarding

- Loan applications

- KYC verification

- Document collection

- Credit bureau checks

- Underwriting

- Risk assessment

- Loan approval workflows

- Sanction generation

- E-signatures

- Loan disbursement

Modern platforms also integrate with Loan Management Systems (LMS), collections software, payment gateways, credit bureaus, and regulatory compliance tools to create an end-to-end digital lending ecosystem.

Why Choosing the Right LOS Matters

The right loan origination platform can dramatically improve lending operations.

Benefits include:

Faster Loan Processing

Automation reduces loan processing times from days to minutes by eliminating manual paperwork and repetitive tasks.

Improved Borrower Experience

Customers expect digital-first lending experiences. Modern LOS platforms enable online applications, document uploads, instant status updates, and digital approvals.

Better Credit Decisioning

Advanced underwriting models and business rule engines improve risk assessment and approval accuracy.

Reduced Operational Costs

Automation significantly reduces staffing requirements and administrative expenses. Some platforms claim lenders can reduce origination and underwriting costs by up to 50%.

Regulatory Compliance

Integrated KYC, audit logs, and compliance workflows help lenders stay aligned with RBI and digital lending regulations.

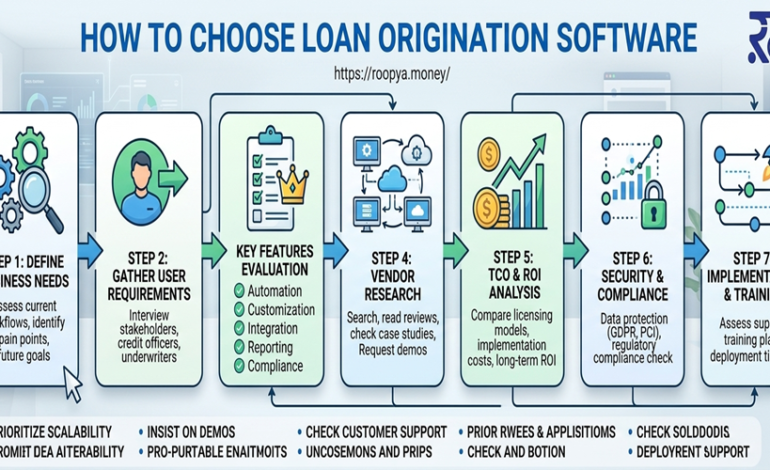

12 Key Factors to Consider When Choosing Loan Origination Software

1. Define Your Lending Business Requirements

Before evaluating software vendors, identify your specific business needs.

Ask:

- What loan products do you offer?

- Personal loans?

- Business loans?

- Gold loans?

- MSME financing?

- Mortgage loans?

- Microfinance loans?

Your LOS should support multiple loan products and allow customized workflows for each lending segment.

2. Evaluate Automation Capabilities

Automation is the primary reason lenders invest in LOS technology.

Look for:

- Automated application processing

- Automated underwriting

- Credit score integration

- Decision engines

- Workflow automation

- Rule-based approvals

- Auto-generated documents

The higher the automation level, the lower the operational cost and turnaround time.

3. Check Digital Borrower Onboarding Features

Borrower onboarding is often the first impression customers have of your lending business.

Choose software that offers:

- Online application forms

- Mobile-friendly applications

- Aadhaar verification

- PAN verification

- OTP authentication

- Video KYC

- E-signature integration

- OCR document extraction

These capabilities improve customer acquisition and reduce abandonment rates.

4. Assess Credit Underwriting Capabilities

Underwriting determines loan quality.

A robust LOS should support:

- Multi-bureau integration

- Credit score analysis

- Income verification

- Banking analysis

- Debt-to-income assessment

- Risk scoring

- Fraud detection

Advanced underwriting tools enable lenders to make data-driven decisions while reducing NPAs.

5. Verify API Integration Ecosystem

Modern lending requires integration with multiple third-party services.

Look for software that integrates with:

- Credit bureaus

- Account Aggregators

- Payment gateways

- Banking APIs

- eNACH providers

- UPI systems

- GST verification

- PAN verification

- Aadhaar services

Platforms with extensive API ecosystems significantly reduce implementation complexity. Roopya, for example, highlights more than 300 pre-integrated APIs for lenders.

6. Evaluate Compliance and Security

Security is critical when handling borrower financial data.

Key requirements include:

- Data encryption

- Role-based access control

- Audit trails

- KYC compliance

- AML compliance

- Data privacy controls

- RBI compliance readiness

A secure LOS protects both lenders and borrowers while reducing regulatory risk.

7. Look for AI-Powered Capabilities

Artificial Intelligence is transforming lending.

Modern LOS solutions offer:

- Automated credit decisioning

- Fraud detection

- Predictive risk scoring

- Behavioral analytics

- Portfolio intelligence

- Early warning signals

AI-driven lending improves portfolio quality and operational efficiency.

8. Check Scalability

Many lenders outgrow their software within a few years.

Ask:

- Can the platform handle increased loan volumes?

- Can it support multiple branches?

- Does it support multiple products?

- Is it cloud-native?

Cloud-based systems provide flexibility, reliability, and growth without infrastructure investments.

9. Review Workflow Customization

Every lender has unique credit policies.

Choose a platform that allows:

- Custom workflows

- Approval hierarchies

- Business rules configuration

- Product-specific journeys

- Multi-level approvals

No-code workflow customization is especially valuable because business teams can make changes without developer involvement.

10. Analyze Reporting and Analytics

Data-driven lending requires visibility.

Look for:

- Real-time dashboards

- Portfolio analytics

- Approval ratio tracking

- Loan funnel reports

- Turnaround time analysis

- Risk reports

- Management information systems (MIS)

Advanced reporting enables continuous optimization of lending operations.

11. Evaluate Vendor Support and Implementation

Software is only as good as its implementation partner.

Questions to ask:

- How long is deployment?

- Is training provided?

- Is onboarding included?

- What support channels are available?

- Is there a dedicated account manager?

Fast implementation reduces downtime and accelerates ROI.

12. Understand Total Cost of Ownership

Many lenders focus only on software licensing costs.

Instead, consider:

- Setup costs

- API costs

- Maintenance costs

- Customization costs

- Training costs

- Upgrade costs

The best LOS is not necessarily the cheapest but the one that delivers the highest long-term value.

Questions to Ask Before Finalizing a Loan Origination Software Vendor

Before signing a contract, ask:

- How quickly can we go live?

- Does the software support our loan products?

- Can workflows be customized?

- What integrations are included?

- Is the platform cloud-based?

- How is customer data secured?

- Does the platform support AI underwriting?

- What compliance features are available?

- What implementation support is provided?

- How does pricing scale as we grow?

Why Modern NBFCs Need Advanced Loan Origination Software

Today’s borrowers expect:

- Instant approvals

- Mobile-first experiences

- Paperless onboarding

- Faster disbursements

- Real-time updates

Traditional lending processes can no longer meet these expectations.

An advanced LOS enables lenders to:

- Increase loan volumes

- Reduce approval times

- Lower operational costs

- Improve borrower satisfaction

- Enhance portfolio quality

- Scale efficiently

Digital transformation is no longer optional; it is a competitive necessity.

Why Roopya is an Ideal Choice for Modern Lenders

Roopya provides a cloud-native, AI-powered Loan Origination Software designed specifically for Indian lenders.

Key capabilities include:

- Digital borrower onboarding

- AI underwriting

- Automated KYC

- Business Rule Engine

- Multi-bureau integrations

- Document management

- Workflow automation

- Loan approval automation

- Analytics dashboards

- End-to-end LOS and LMS platform

The platform supports NBFCs, banks, fintech companies, MFIs, and digital lenders looking to automate and scale their lending operations.

Choosing the right Loan Origination Software is a strategic investment that affects every aspect of lending operations. The ideal platform should provide automation, compliance, scalability, AI-powered decisioning, seamless integrations, and an exceptional borrower experience.

Before selecting a vendor, carefully evaluate your business requirements, future growth plans, and technology ecosystem.

Lenders that invest in the right LOS today will be better positioned to increase operational efficiency, reduce risk, improve customer satisfaction, and achieve sustainable growth in the rapidly evolving digital lending landscape.

FAQ

Q1. What is Loan Origination Software?

Loan Origination Software is a digital platform that automates loan application processing, borrower onboarding, underwriting, approvals, and disbursement.

Q2. Why is Loan Origination Software important for NBFCs?

It improves efficiency, reduces operational costs, speeds up approvals, enhances compliance, and improves borrower experience.

Q3. What features should I look for in a Loan Origination System?

Look for automation, KYC integration, AI underwriting, workflow management, API integrations, reporting, compliance tools, and scalability.

Q4. Is cloud-based Loan Origination Software better?

Yes. Cloud-based systems offer scalability, remote access, lower infrastructure costs, and faster deployment.

Q5. Can Loan Origination Software integrate with credit bureaus?

Yes. Modern LOS platforms integrate with CIBIL, Experian, CRIF, Equifax, and other credit data providers.

Q6. How does AI help in loan origination?

AI improves underwriting, fraud detection, risk assessment, and automated decision-making.

Q7. How long does LOS implementation take?

Implementation varies by vendor. Some modern no-code platforms can be deployed in as little as one day.

Q8. Who should use Loan Origination Software?

NBFCs, banks, fintech companies, cooperative banks, MFIs, and digital lenders.